New IEEFA Report Warns Massive Financing Gap Could Slow EV Transition Unless Structural Reforms Follow

India’s electric vehicle (EV) industry one of the fastest-growing sectors in its clean mobility push has attracted significant capital over the past five years. However, a new analysis by the Institute for Energy Economics and Financial Analysis (IEEFA) reveals that about ₹2.23 lakh crore has been invested in EVs from 2020 to 2025, representing only 18 per cent of the total capital required to hit the nation’s electrification targets by 2030.

The findings highlight a substantial investment shortfall that industry experts warn could derail India’s ambitious goals for EV adoption unless policymakers and private investors adopt structural financing reforms. According to the report, 82 per cent of the required capital, estimated at ₹12.5 lakh crore, still needs to be mobilised in the next five years to support EV manufacturing, charging infrastructure, and the broader ecosystem.

EV Investment Growth and the 2030 Target

India’s 2030 electrification roadmap aims for 30 per cent of private cars, 70 per cent of commercial vehicles, 40 per cent of buses, and 80 per cent of two- and three-wheelers to be electric. Achieving these milestones will require robust capital flows across manufacturing, infrastructure, and financial ecosystem support.

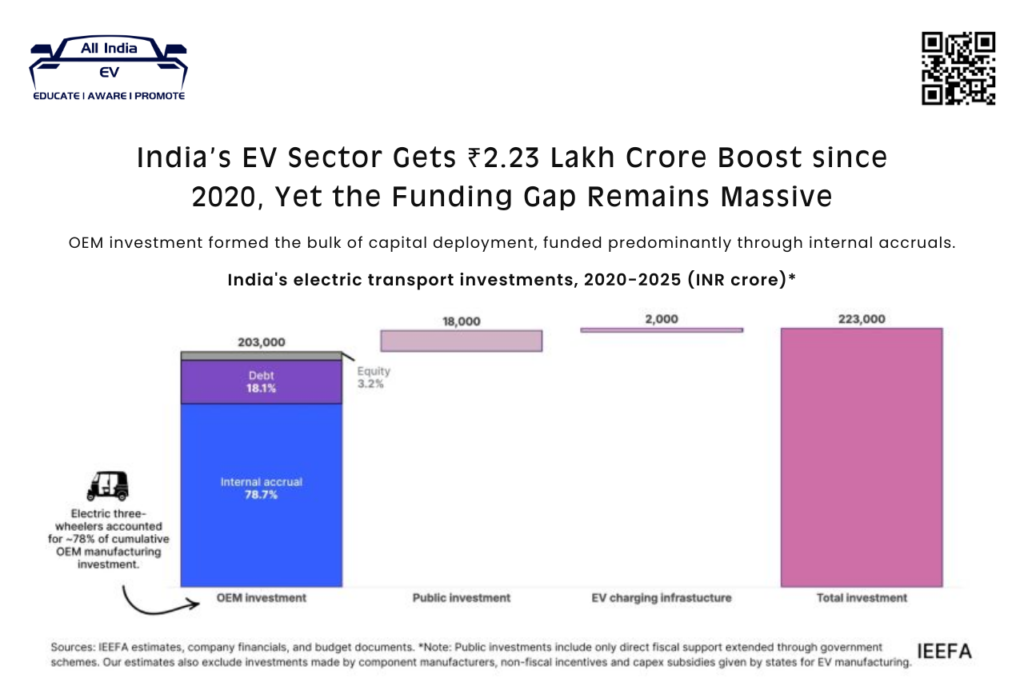

The IEEFA report, titled Capital Flows in India’s Electric Transport Sector, is the first consolidated analysis of realised EV investments over five years. It reveals that cumulative inflows while significant in nominal terms fall well short of the scale needed for sustained growth. From 2020-2025, total capital deployed in the EV segment was around ₹2,23,119 crore (about USD 25.6 billion), covering three core areas: manufacturing capacity, public subsidies and incentives, and EV charging infrastructure.

Where the Money Went: Manufacturing Takes the Lead

A breakdown of investment patterns shows that EV manufacturing attracted the lion’s share of capital between 2020 and 2025. Within that, internal accruals accounted for the largest portion, totalling roughly ₹1.6 lakh crore. Debt financing contributed another ₹36,738 crore, while equity infused about ₹6,455 crore into manufacturing.

Sector analysts say this funding mix reflects the cumulative strength of established manufacturers and the relatively limited participation of external investors in newer segments. Notably, the electric three-wheeler segment among the earliest and most mature parts of the EV market captured roughly 78 per cent of investments due to its fragmented OEM base and low capital intensity.

More EV News

In contrast, segments such as four-wheelers and two-wheelers have seen a gradual shift in capital flows in 2024-2025, driven by rising consumer demand for premium electric cars and high-performance personal mobility options.

Charging Infrastructure: A Critical Gap

While manufacturing has drawn most attention, investment in public charging infrastructure has lagged significantly. India’s publicly accessible charging network has expanded from around 5,151 chargers in 2020 to nearly 39,485 by 2025, signalling growth but remaining far below global benchmarks in charger-to-EV ratios.

IEEFA estimates that approximately ₹20,600 crore is required to build enough charging infrastructure to support 2030 goals yet, only about 9.6 per cent of this has been invested so far. This gap threatens to constrain EV usage and undermine consumer confidence, experts warn.

High Financing Costs Erode EV Advantage

One of the most pressing barriers identified by the report is costly commercial financing. EV businesses and fleet operators typically face interest rates ranging from 15 per cent to 33 per cent, sharply eroding the economic case for adopting electric fleets. This high cost of capital, analysts say, diminishes the total cost-of-ownership advantage that EVs typically offer and slows fleet expansion and manufacturing investment.

IEEFA’s co-authors highlight that the core issue is not a lack of capital in the financial system but how EV sector risk is priced by lenders, who remain cautious due to uncertainty around battery performance, residual values, and cash-flow predictability.

Proposed Solutions: Finance Innovation Needed

To bridge the ₹10.3 lakh crore gap left to be filled by 2030, IEEFA proposes the creation of an integrated EV financing platform. The platform would bundle tools such as partial credit guarantees, residual value protections, battery-as-a-service models, and co-lending frameworks to reduce risk for lenders and align incentives across stakeholders.

The report suggests specialised development finance institutions could anchor this platform for example, SIDBI focused on MSME and small fleet finance, and IIFCL for larger commercial vehicle deployments.

Experts argue that lower financing costs would stimulate demand, strengthen revenue visibility, lower risk premiums, and attract new private capital creating a virtuous cycle of investment and deployment.

Outlook: From Subsidy-Driven to Self-Sustaining Growth

India’s EV evolution is poised at a critical inflection point, with strong policy impetus and growing consumer interest but significant investment barriers still to be addressed. Without structural changes in financing models, analysts caution, the country may struggle to convert its electrification aspirations into reality by 2030.

The IEEFA report underscores that the transition to electric mobility will increasingly hinge on innovative financing solutions, private sector participation, and risk-sharing mechanisms not just government subsidies in steering India’s clean transportation future.