How India Built the World’s Largest Three-Wheeler Market — And Why the World Is Only Now Paying Attention

When the global EV conversation kicked into high gear around 2017–18, the obsession was singular: passenger cars. Tesla’s Model 3. Volkswagen’s ID.4. BYD’s ambitions. The metric everyone tracked was four-wheeled, middle-class, highway-range-capable.

- How India Built the World’s Largest Three-Wheeler Market — And Why the World Is Only Now Paying Attention

- Phase 1: 1990 – 2005 – The Accidental Infrastructure

- Phase 2: 1990 – 2005 – Global Context

- Phase 3: 2009 – 2015 – Policy Discovers the Segment

- Phase 4: 2015 – 2019 – FAME I and the First Real Electrification Push

- Phase 5: 2019 – 2022 – FAME II, State Policy Wars, and the Making of a Real Market

- Phase 6: 2022 – 2024 – When the Economics Took Over

- Phase 7: 2024 – Present – The Global Players Arrive — Into a Market They Did Not Build

- What India Built That Others Cannot Quickly Copy

- Three Tensions That Will Define the Next Decade

- The Market the World Missed

India’s three-wheeler market — noisy, unorganised, stuffed with CNG and diesel engines, carrying anything from school children to fish boxes — was, in that framing, an afterthought.

That was the mistake.

While the world modelled EV adoption through the lens of the passenger sedan, India was quietly running the world’s largest natural experiment in commercial electric mobility — in a segment with higher daily utilisation, lower battery requirements, faster payback periods, and deeper social penetration than any four-wheeler would ever achieve.

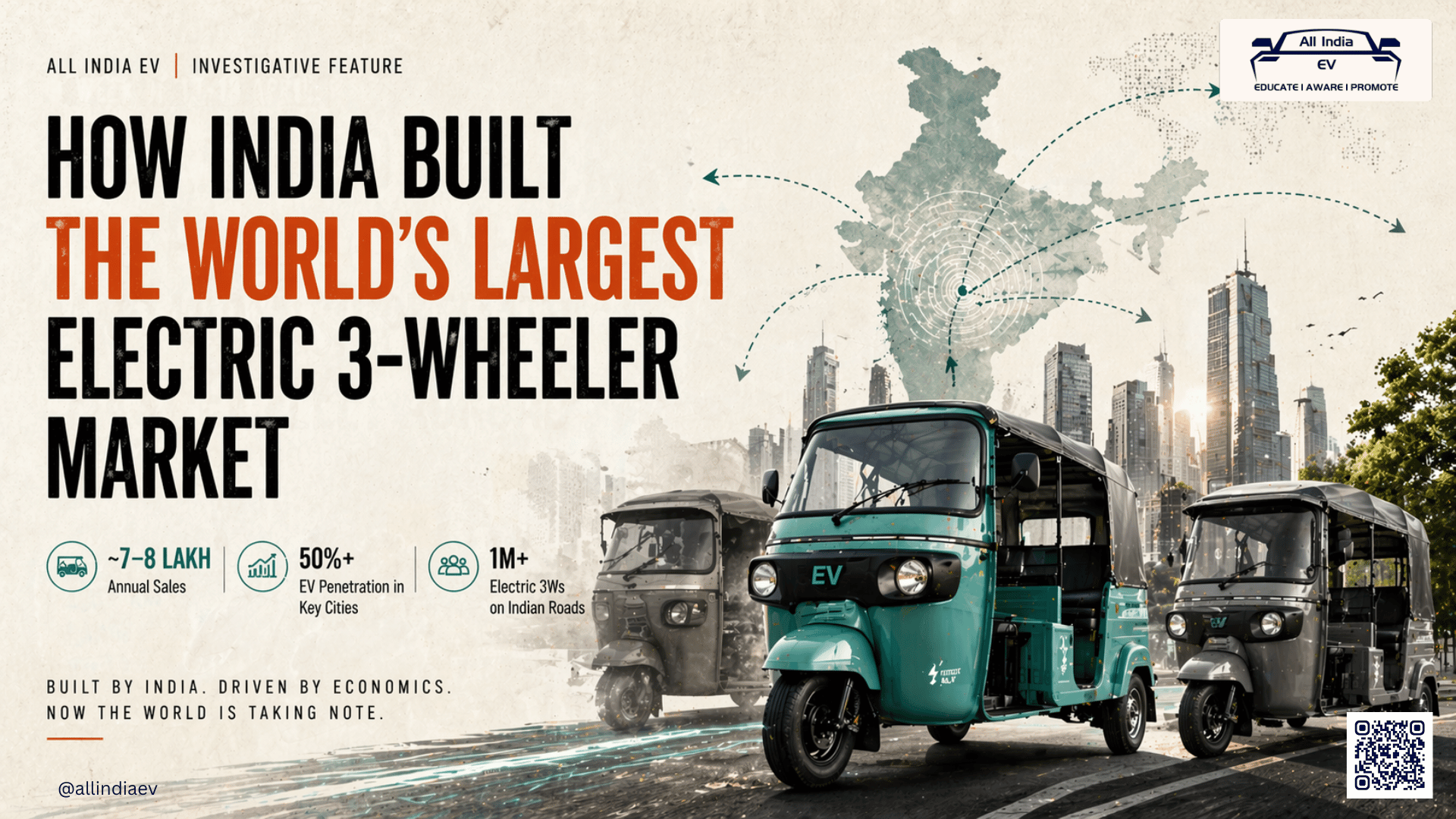

Today, India sells between 7 and 8 lakh three-wheelers annually. Electrification in the segment is not a story of ambition. It is a story of arithmetic. And the arithmetic, in many cities, already favours electric over ICE — with or without government subsidy.

To understand why this happened here, and not in Indonesia, Brazil, or Nigeria — all of which share similar urban density and last-mile mobility gaps — you need to go back to the beginning. The answer is not technology. It is not policy alone. It is the collision of structural demand, informal innovation, and a driver community that made economic decisions faster than any government scheme ever could.

Phase 1: 1990 – 2005 – The Accidental Infrastructure

The 1990s liberalisation unlocked Indian cities. It did not, however, unlock the infrastructure those cities needed. Public bus networks were underfunded and route-constrained. Personal vehicles were aspirational but unaffordable for the median urban household. The gap between the two — what urban planners now call the “last-mile problem” — was vast, visible, and economically exploitable.

Auto-rickshaws filled it. Not because any planner decided they should. Because they could.

More EV News

— Why Auto-Rickshaws Won the Streets

→ Low purchase cost: relative to cars — accessible to first-generation urban migrants with limited capital

→ High manoeuvrability: in congested, narrow city lanes that buses could never navigate

→ No route licensing: in most cities — unlike buses, autos could serve any origin-destination pair

→ Fare affordability: priced for the working class, not the aspirational middle

→ Self-employment model: no corporate backing needed, minimal barrier to entry

By the mid-1990s, the auto-rickshaw was not merely a mode of transport. It was an employment category, a social institution, and — without anyone articulating it as such — a distributed urban mobility network operated entirely by small entrepreneurs with no corporate backing and no government mandate.

By the early 2000s, India had become one of the largest three-wheeler markets in the world — not through policy, but through the absence of alternatives.

Phase 2: 1990 – 2005 – Global Context

→ China: Focused on bicycles and the early e-bike boom. Electric 3Ws existed as rudimentary lead-acid cargo carriers in rural provinces — not yet a commercial or export story.

→ Africa: Paratransit ecosystems (tuk-tuks, bajaj, kekes) were growing but fragmented. No country had cracked commercially viable electric 3Ws at scale.

→ India’s unique edge: Not electrification — but market depth. No other country had built a comparable last-mile, commercially operated 3W network across this many cities and use cases.

India’s early lead was invisible to global EV strategists in 2005. They were watching Detroit and Munich. Nobody was watching Kanpur or Patna. That studied ignorance of informal mobility systems would cost the global EV industry a decade of insight it never got back

Phase 3: 2009 – 2015 – Policy Discovers the Segment

The first national EV push was not about three-wheelers. Three-wheelers adopted it anyway.

The 2009 National Mission on Electric Mobility (NEMMP) was a broad-spectrum policy targeting a range of vehicle categories and setting an ambitious headline number — 6 to 7 million EVs on Indian roads by 2020. In retrospect, the target was fantastical. But the policy conversation it opened was consequential.

— Why Three-Wheelers Became the Natural Entry Point

- Battery requirement: A typical auto-rickshaw operates within a 100–150 km daily range. The pack required is a fraction of what a passenger car needs — reducing upfront cost and technology risk dramatically.

- Route predictability: Commercial 3Ws operate on known urban corridors. Charging infrastructure did not need to be ubiquitous — just placed at specific, known points.

- Driver economics: Fuel cost is an existential variable for a driver whose daily margin is already thin. Lower per-km running costs were not an abstract benefit — they were the difference between financial survival and distress.

- Regulatory leverage: City governments could mandate electric 3Ws for specific permit categories — particularly in CNG-regulated cities where ICE auto permits were already being restricted.

The e-rickshaw didn’t wait for policy to arrive. It arrived before policy could stop it — and forced the government to catch up.

— The E-Rickshaw Wildcard Nobody Planned For

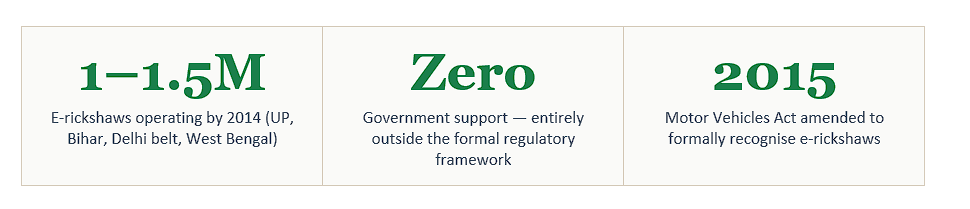

Between 2009 and 2015, a development occurred that no policy document anticipated: the mass, informal adoption of the e-rickshaw in North India. These were not the product of NEMMP. They were the product of Chinese battery technology becoming cheap enough for small Indian assemblers to build a functional electric vehicle for ₹80,000–1,00,000 — within reach of drivers who could never afford a CNG auto.

Phase 4: 2015 – 2019 – FAME I and the First Real Electrification Push

AME I did not electrify the three-wheeler market. It legitimised the electrification that was already happening.

The Faster Adoption and Manufacturing of (Hybrid and) Electric Vehicles scheme — FAME I — launched in April 2015 with a ₹795 crore outlay. For three-wheelers, it provided demand incentives: per-vehicle subsidies that made electric options more price-competitive at the point of purchase.

— What FAME I Actually Did to the Market

→ Low-speed segment: worked most powerfully for e-rickshaws and e-carts where the price differential was already narrow

→ Higher-spec OEMs: created conditions for product-market fit conversations with players like Mahindra and Piaggio

→ Entry triggered: hundreds of small manufacturers entered the market — with varying degrees of engineering rigour

→ Mass adoption: lower entry barriers drove adoption in Tier-2 and Tier-3 cities at previously unseen pace

India paid a reputational price for the informal e-rickshaw boom — but gained mass-market deployment data at a scale no other country had accumulated.

— The Quality Problem Nobody Wants to Discuss

This period produced India’s first major EV quality crisis in the three-wheeler segment. Fire incidents, battery failures, and structural integrity issues with unbranded e-rickshaws created a narrative that threatened to discredit the entire category.

→ Government response: tighter BIS standards, mandatory testing, phased AIS specifications for electric 3Ws

→ Implementation: slow, contested by informal sector interests, imperfectly enforced

→ Net outcome: the process of formalising quality expectations that would define the FAME II era had begun

Phase 5: 2019 – 2022 – FAME II, State Policy Wars, and the Making of a Real Market

FAME II did not just fund EVs. It restructured the competitive landscape of Indian EV manufacturing.

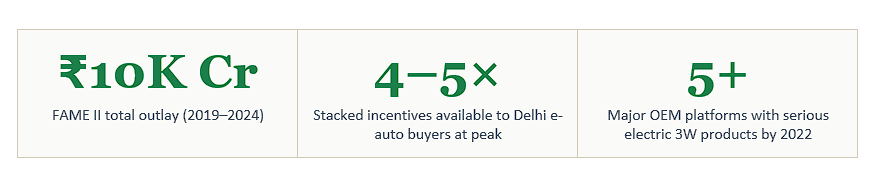

FAME II — ₹10,000 crore, launched April 2019 — was architecturally different from its predecessor. It was not a broad-based demand subsidy. It was a targeted intervention designed to produce specific, verifiable outcomes.

— Three Provisions That Changed Everything

- Localisation requirements: Subsidies were conditional on minimum locally-sourced component percentages — progressively tightened over the scheme’s life. This single provision restructured the supply chain politics of the entire segment.

- Commercial vehicle priority: FAME II explicitly prioritised electric buses and commercial three-wheelers over private passenger vehicles — betting on high-utilisation vehicles to generate visible proof of EV economics.

- Fleet aggregator catalysis: The commercial focus enabled lease-to-own models and battery-as-a-service arrangements that addressed the primary adoption barrier: high upfront cost relative to an ICE alternative.

— The State Policy Multiplier Effect

Simultaneously, state governments began competing with each other on EV policy ambition. Delhi, Maharashtra, UP, Gujarat, and Karnataka each launched distinct policy architectures calibrated to local political economy.

A driver in Delhi switching from a CNG auto to an electric 3W in 2021 could access FAME II subsidy, Delhi state subsidy, a scrappage incentive, and a preferential permit simultaneously. At that stacking, the question was not whether to switch. It was only when. Policy, when designed to compound, does not nudge — it tips.

🌐 Global Context: When Capital Started Looking at India

→ IFC, ADB, climate funds: Began taking positions in Indian e-3W companies. India had a proven deployment market, genuine policy tailwind, and unit economics approaching a tipping point.

→ China’s absence: Chinese OEMs were not natural competitors in India’s passenger-carrying 3W segment

→ China’s urbanisation had skipped this vehicle category, going directly to e-bikes and cars.

→ India’s window: For a brief but important period, India had the passenger electric 3W market largely to itself. The competitive gap was real and wide.

Phase 6: 2022 – 2024 – When the Economics Took Over

The most dangerous moment for a subsidy-driven market is when the subsidies become irrelevant. India’s 3W market reached that moment — and kept growing anyway.

The FAME II scheme ran into turbulence in 2023. A misuse investigation triggered a policy crisis, with disbursements slowing for months. The scheme’s future was uncertain.

What happened to three-wheeler adoption during this period? It continued growing.

When subsidies disappeared and the market didn’t flinch — that was the moment India’s e-3W story stopped being a policy story and became an economic inevitability.

| Cost Factor | CNG Three-Wheeler | Electric Three-Wheeler | EV Advantage |

| Per-km running cost | ₹2.8 – 3.5 | ₹1.4 – 1.8 | 30–40% lower |

| Daily fuel / energy | ₹350 – 450 | ₹150 – 220 | ~₹200 saved per day |

| Monthly fuel saving | Baseline | — | ₹4,000 – ₹8,000 |

| Maintenance cost | Higher (engine, exhaust) | Lower (fewer parts) | Significant edge |

| Daily utilisation | 8–12 hrs | 8–12 hrs | Equal |

| Permit access | Restricted / expensive | Priority / subsidised | Structural advantage |

— The Driver Network Effect: Social Proof as Adoption Engine

A development often overlooked in top-down policy analysis is the role of the driver community in normalising electric 3Ws. Informal knowledge networks — caste associations, cooperative societies, union networks — began transmitting information about real-world running costs, charging logistics, and maintenance experiences.

New drivers were choosing electric not because of a government mandate, but because the driver parked next to them was making more money on the same route. This social proof mechanism is not something any policy document designed.

Phase 7: 2024 – Present – The Global Players Arrive — Into a Market They Did Not Build

When Hyundai, global logistics players, and development finance institutions begin seriously looking at India’s e-3W segment, they are not pioneers. They are late entrants to an Indian-built ecosystem.

The past eighteen months have seen a qualitative shift in global attention to India’s three-wheeler market. This is no longer a development finance conversation. It is a commercial strategy conversation.

— Three Developments That Forced Global Attention

- Proof of scale: India has demonstrated that over a million electric three-wheelers can operate commercially and profitably in a complex urban environment. This proof does not exist at equivalent scale anywhere else.

- Export market logic: Africa’s urban mobility market — Nigeria, Kenya, Ethiopia, Egypt, Uganda — runs on three-wheelers. These markets are where India was in 2010. Indian OEMs are now positioning there, mirroring China’s Africa strategy a decade ago.

- Southeast Asian replication interest: Thailand, Vietnam, and Indonesia are watching the Indian 3W electrification model. The Indian playbook — informal adoption, policy legitimisation, OEM consolidation, subsidy sunset — is being studied as a potential replication model.

When Hyundai signals interest in India’s 3W space, it is not creating a market. It is confirming that the market risk has already been retired — by India.

— Global Electrification Comparison: Who’s Where

| Country / Region | 3W Market Scale | EV Penetration | Key Barrier | Status |

| 🇮🇳 India | 7–8 lakh/year | 35–50%+ (key cities) | Battery cell localisation | Market Leader |

| 🇧🇩 Bangladesh | Large (informal) | High (lead-acid corridors) | No domestic manufacturing | Informal Only |

| 🇳🇬 Nigeria | 500K+ keke units | <5% | Financing + infrastructure | Early Stage |

| 🇰🇪 Kenya | Growing | <10% | Grid reliability + cost | Pilot Scale |

| 🇹🇭 Thailand | Moderate (tuk-tuk) | <5% | No policy urgency | Watching India |

| 🇨🇳 China | Large (cargo-focused) | High (cargo/rural only) | Passenger 3W not prioritised | Export Play |

| 🇪🇬 Egypt | Large (tuk-tuk) | <2% | Subsidy dependence + imports | Nascent |

— The China Question: India’s Supply Chain Vulnerability

The most consequential global variable in India’s 3W story is the one least discussed in domestic policy circles: India’s battery cell dependency on China.

→ Cell sourcing: Majority of lithium-ion cells powering Indian electric 3Ws are from Chinese manufacturers: CATL, BYD, CALB, and second-tier suppliers

→ Pack vs. cell: Indian assemblers domesticate supply at the pack level — cell-level independence is a decade away at minimum

→ PLI timeline: Ola Electric, Reliance-backed entities investing in cell manufacturing — but commercial-scale output unlikely before 2026–28

What India Built That Others Cannot Quickly Copy

The three-wheeler electrification story is often narrated as a demand story. But the deeper story is an ecosystem story — one that took thirty years to construct and cannot be replicated in thirty months.

| 1. Manufacturing Depth India now has multiple OEMs building electric 3Ws with genuine engineering capability, warranty programs, and service networks. This happened because market volume created the commercial case. Replicating this in another market requires years of demand accumulation before the supply side responds equivalently. |

| 2. Driver Knowledge Networks The social infrastructure of the driver community — associations, cooperatives, informal information networks — has become a powerful adoption accelerator. New drivers learn from experienced e-auto drivers, not from government campaigns. This social proof mechanism is not exportable. |

| 3. Financing Infrastructure India’s NBFC ecosystem, microfinance institutions, and formal banks have developed 3W-specific EV loan products. The underwriting models, risk frameworks, and recovery infrastructure have been built through years of market experience. Other markets are still at the beginning of that curve. |

| 4. Regulatory Sophistication India has gone through multiple iterations of type certification, safety standards, charging regulation, and permit policy for electric 3Ws. The learning curve was steep and costly — but it produced a framework that provides sufficient certainty for serious investment. Other markets are still at the start. |

Three Tensions That Will Define the Next Decade

India tends to celebrate what it has built and delay the conversation about what could undo it. The three-wheeler market deserves both the celebration and the hard questions. Here are the three it cannot avoid.

— Tension 1: Formalisation vs. Informality

The informal e-rickshaw sector — now estimated at over 1.5 million units in operation — remains largely outside the formal OEM and regulatory framework. Formalising this sector through retrofit programs, scrappage incentives, and financing access represents both a market opportunity and a policy challenge. How India manages this transition will determine whether the next 10 million electric 3Ws are built on quality foundations or replicate the safety problems of the informal era.

— Tension 2: Battery Localisation

The cell manufacturing gap is India’s most significant supply chain vulnerability. The risk is precise: India builds global leadership in 3W EV deployment while remaining structurally dependent on imported cells — vulnerable to supply disruptions, currency volatility, and geopolitical friction. PLI-backed investments are real. Timelines are uncertain. The technical gap is significant.

— Tension 3: Export Ambition vs. Domestic Priority

Indian 3W OEMs are increasingly positioned to compete in African, Southeast Asian, and South Asian export markets. But export growth requires capital, capacity, and management bandwidth that domestic market growth also demands. The companies that navigate this tension well — prioritising export markets where Indian vehicles have genuine competitive advantage — will define the next chapter of the story.

The Market the World Missed

India did not become the world’s largest three-wheeler EV market because of one policy, one company, or one technology breakthrough. It became the world’s largest three-wheeler EV market because of an accumulation — of structural demand, informal innovation, formal policy reinforcement, OEM investment, driver community adoption, and finally the irreversible logic of unit economics.

The global EV industry spent the 2010s focused on the wrong segment. The high-margin, high-profile passenger car market absorbed the headlines, the venture capital, and the policy attention. Meanwhile, India was running the largest real-world deployment test of commercial electric mobility in history — in a vehicle category that moves more people daily, at more economically significant utilisation rates, than any private sedan ever will.

When global players look at India’s 3W market today — with admiration, with investment interest, with export anxiety — they are looking at the result of thirty years of construction. Some of it was planned. Most of it was adaptive. All of it was Indian.

The lesson for every market still waiting for the right policy before committing to electrification: the market does not wait. In India, it never did.

Read More: Catch up on All India EV’s related coverage on India’s evolving commercial EV subsidies and battery swapping policies at All India EV